[ad_1]

FG Business Latin/E+ via Getty Images

fuboTV Inc.Nice: Fubo) caught my attention after I came to the public market because the company is operating in an impressive segment of the open streaming market and riding the macro. Tendency to cut the cord. But I was never interested in owning the shares because the price had quickly ballooned to astronomical levels, making any investment case study completely unrealistic.

With shares down 92% from their February 2021 highs, I thought it would be interesting to take a second look at the company and see if it’s a bet worth taking.

Overall, the business is still growing well but has not reached any economic level. To make matters worse, FuboTV is still operating at a negative gross margin, has a troubled balance sheet, and is on an uncertain path to profitability. I doubt the company knows a sustainable way to do it, and there’s a good chance Fubo will go out of business. Not my favorite bet, but let’s take a closer look at why the company has so many issues.

The wrong business model in a strong market

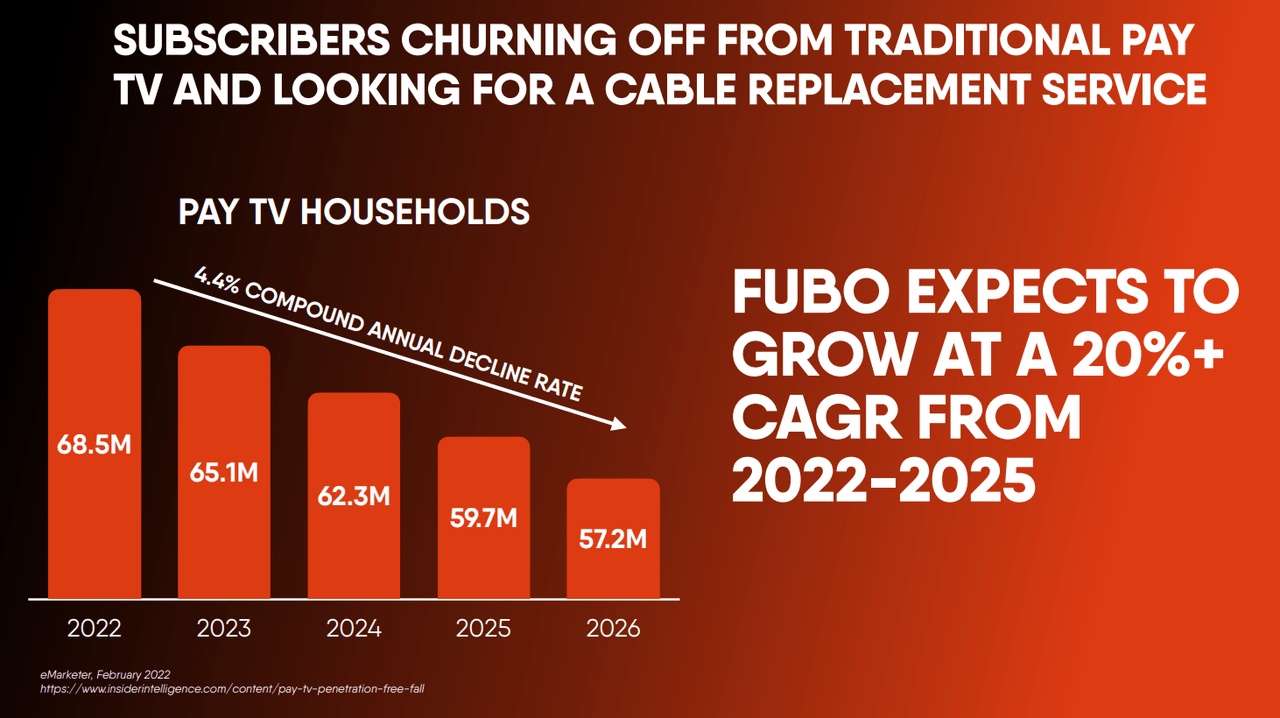

Fubo is a streaming service dedicated to live TV and sports productions. The business is trying to capitalize on cord-cutting trends, primarily in the United States, where over the past decade more and more consumers have ditched traditional cable or satellite subscriptions in favor of generally cheaper and more user-friendly streaming services.

When it first started, Fubo offered primarily sports that didn’t appeal to many customers, offering itself at an incredibly low price ($7 per month). Over the years, the company has begun to offer more and more channels and now the price is starting at $69.99, which is much higher than in the past, but still lower than some traditional offerings.

FUBO Investor Day Presentation – eMarketer data

The main problem with Fubo’s business is that essentially all of the money coming in through subscriptions for sports rights has to be given almost entirely to content owners. This makes Fubo’s business inherently low-margin if it isn’t supported by additional revenue streams that aren’t strictly on visible content.

On this topic, the latest Q2 2022 earnings report shows that the company is improving its ad business (+32% YoY), but at the same time the average revenue per user (ARPU) per user decreased by 18% to $7.25. The ad business is starting to reach exciting levels ($21.7 million in the last quarter) as this additional revenue stream helps the platform grow its gross margin meaningfully. However, most of Fubo’s growth appears to be in the “Rest of the World” user segment, which has far lower incomes than North America. As of last quarter’s report, Fubo had 947,000 customers in NA and 347,000 ROW, but generated $5.8 million in revenue from ROW customers alone (less than 3% of total revenue).

It will be a critical question if Fubo can successfully monetize all of its customers outside of North America. However, the road is uphill, especially through advertising. Meta Platforms (META) and Pinterest (PINS) are examples of many large businesses that have always struggled to grow their ROW ad ARPU to US levels, so I can’t say I’m optimistic at this stage considering the perils on Fubo’s path. moment.

In addition to advertising revenue, Fubo announced the launch of Fubo Sportsbook in Iowa in 2021. The idea was to combine live TV with an interactive platform that would allow customers to stream the games in real time. Unlocking has been embraced by the market as an additional way to generate profitability away from direct reliance on licensed content. Fast forward just one year, and the company recently announced a strategic review of the project, because it was too expensive to produce at home. The company will evaluate how to move forward with the partnership. The only thing that is certain is that betting is far from making any meaningful contribution to Fubo’s profits.

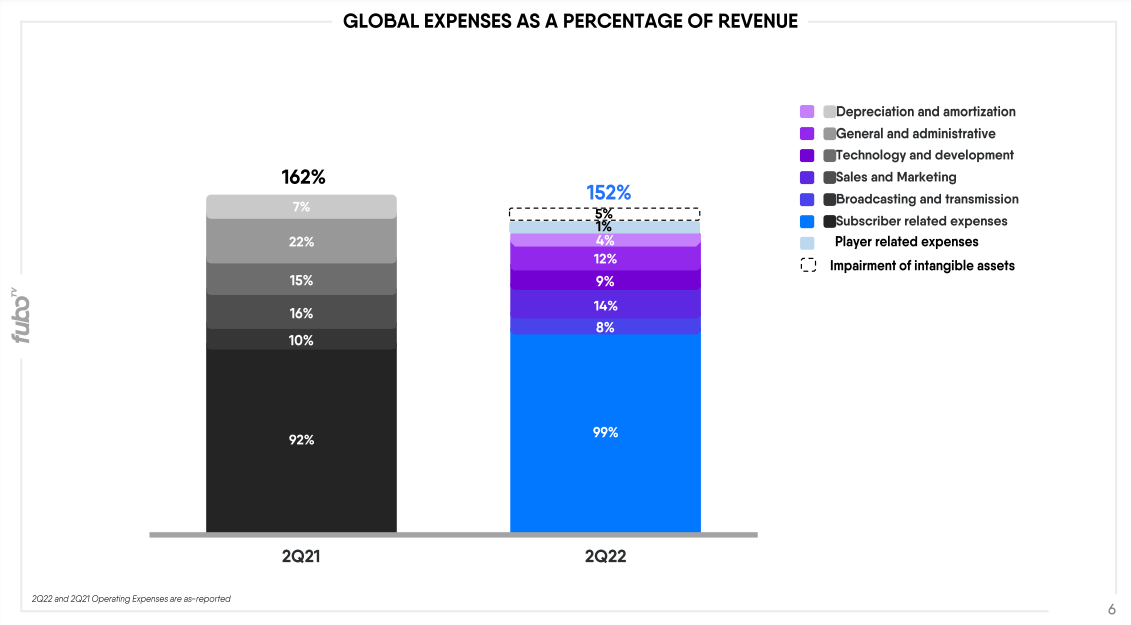

The question with Fubo is if the company can fix its unsustainable business model. As shown in the slide below, the company is still spending more than it brings home to operate. Of particular concern are the “expenses related to subscribers” structural to the business, their impact on total revenue, increased from 92% in the current quarter to 99% in 2Q 2021. The result is a big loss that’s growing YoY: From a loss of $94.4 million in the same quarter last year, the company now reports a loss of $172.4 million on revenue of $221 million.

Fubo Q2 2022 Earnings Report

A company’s balance sheet does not provide a sustainable cushion for uncertain times ahead. The company has $372 million in cash and short-term investments and $392 million in long-term debt, and it burns through cash quarter after quarter. After going public, the company must post a quarter of its operations in cash, which means the company needs to raise money at some point. But we are no longer in 2021, when stock prices are sky high and the cost of capital is historically cheap. Raising money is expensive for the company and for existing shareholders it would be more expensive if management were to launch secondary offerings.

Some progress in the future, but it may not be enough

Although at a slower pace compared to the past, the company is still leading the growth of the number of customers: in 2022, Fubo estimates 1.3 million customers, compared to the 1.13 million registered in February 2021 (approximately 15%) . A long-term forecast presented at the company’s investment day in August projected a CAGR of 15% subscriber growth until 2025, when Fubo hopes to reach the 2 million subscriber milestone.

Despite the growth seen in the past, the financial position of the company is still very serious. The company is still posting negative gross margins of -6.38%, which is a scary place to be in any business. Fubo is operating in a particularly highly competitive market, which generally requires high operating costs as well as the need to support the company’s profitability (or rather, survival) and acquire customers. Fubo may be one of the few players in town in streaming live sports, but in reality the company competes head-to-head with all kinds of rivals like Netflix ( NFLX ) , Disney+ ( DIS ) in the per-view category of streaming. , HBO max and many more.

A company with a fundamentally broken business model is difficult to assess at its current level. Fubo has no earnings or free cash flow (or positive cash flow) to compare to competitors of its size. Fubo is literally fighting for its survival and is betting everything from advertising or sportsbook ancillary revenue to play well in the future. Basically there are no parameters for shareholders to estimate such a business because the current model is unsustainable. One can argue that the P/S of 0.69 is cheap, especially compared to historical values. However, at the current run rate this seems too expensive for my taste, considering that the company will soon need to raise cash or go out of business.

I can see a future where Fubo manages to reach a large enough user base to monetize the platform through advertising and use additional revenue streams to support its existence. If that happens, we’ll look at the stock trading at $3.69 again and regret not buying. I can also see many futures where the company doesn’t attract enough users, isn’t able to increase ARPU to non-US customers, and doesn’t have any pressure on its competitors to see price increases. This looks like a more likely future to me, and as such, I wouldn’t recommend anyone owning the stock at this level.

[ad_2]

Source link